A minor but nonetheless significant part of addressing the housing supply has been filled by the taxpayer-funded Approved Housing Bodies (AHB.)

These are voluntary non-profit housing associations which are enabled under the 1992 Housing Act to finance the building of affordable housing.

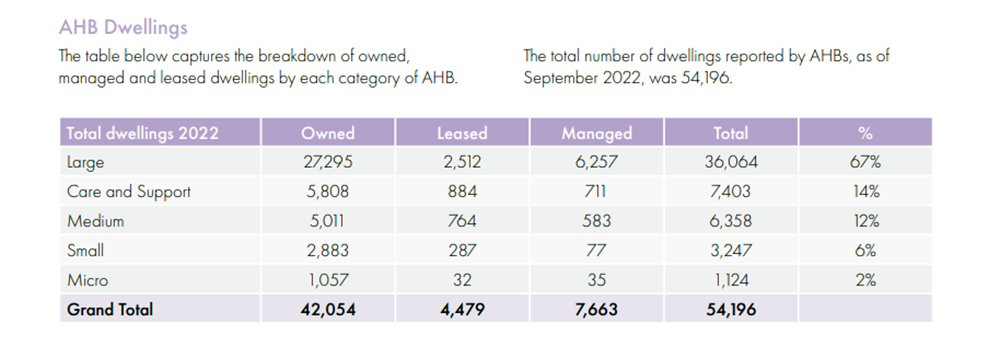

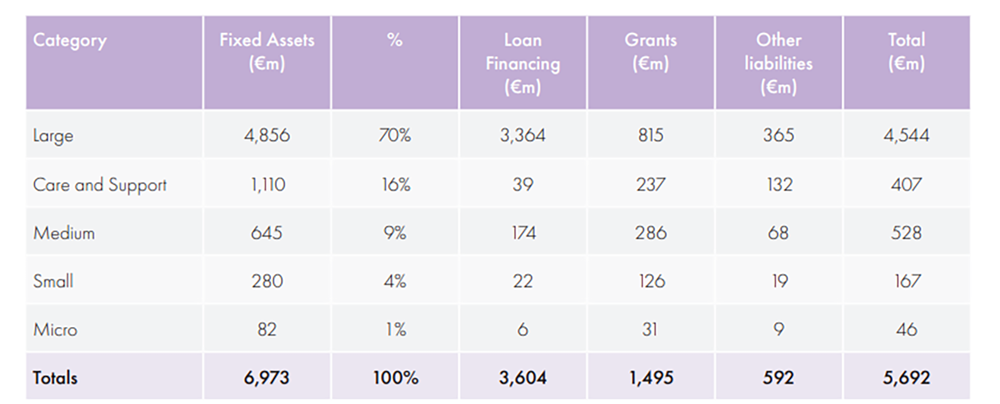

The six largest of the 450 AHBs which form the Housing Alliance now claim to be responsible for 30,000 such homes. The sector as a whole owns and manages 54,196 homes and has around €7 billion in assets. The largest AHBs – 32 of them are responsible for 100 or more homes and just 8 of those for more than 1,000 – control the greater bulk of the housing stock.

Much of the AHBs finance has come through the Capital Assistance Scheme (CAS) directly through the local authorities.

However, more recently financing has come through the Capital Advance Leasing Facility (CALF) which allows forlong term loans either from local authorities and from the state Housing Finance Agency (HFA) or directly through private commercial loans.

Has the greater flexibility in financing perhaps led to a situation as recently reported that the AHBs are now facing a serious debt crisis?

According to a document seen by the Irish Times Clúid warned the Department of Housing last year that the level of debt carried by Clúid and other AHBs was threatening to undermine their ability to meet their targets, and thereby contribute to a shortfall in the state’s target for new homes.

In its financial report for 2022, Clúid stated that it had borrowed €361 million through the various schemes.

A 2021 report in the Sunday Business Post referred to Clúid’s plans to raise finance from pension funds but their 2022 annual report and financial statement does not specifically refer to whether any of these or other private sources accounted for part of the monies borrowed.

Clúid had previously agreed a €54 million loan with the UK firm Legal and General Group. Part of that was used to finance the building of 40 apartments in the Dublin suburb of Raheny in 2021. Fiona Cormican who was then business director at Clúid and now runs her own consultancy business justified the new departure on the basis that it would save taxpayers money. She pointed to the availability of finance from “a ready market of investors willing to invest” in the Irish market.

Which is all well and good, but the loans do have to be repaid, and what are the potential penalties should the accumulating debts become such a burden that it raises the possibility of having to cede control of housing assets to those private financiers?

Clúid’s 2022 financial statements show that the housing body has €1.9 billion in Assets and €1.7 billion in liabilities – and only €38 million in cash and bank. With the sharp rise in interest rates causing a crisis for mortgage holders, can AHBs sustain these huge levels of debt?

Nor is it the case that Clúid’s dependency on the taxpayer has declined. In 2019 it had a total income of €61.1 million of which €38.7 million or 63% came from public funding. In 2022 Clúid had an income of €109.1 million and received €75.5 million in tax funding.

The Directors Report for 2022 did refer to the fact that they were “evaluating the current Public Private Partnership opportunity, stock transfer opportunities, and the introduction of the active portfolio management into our way of working.”

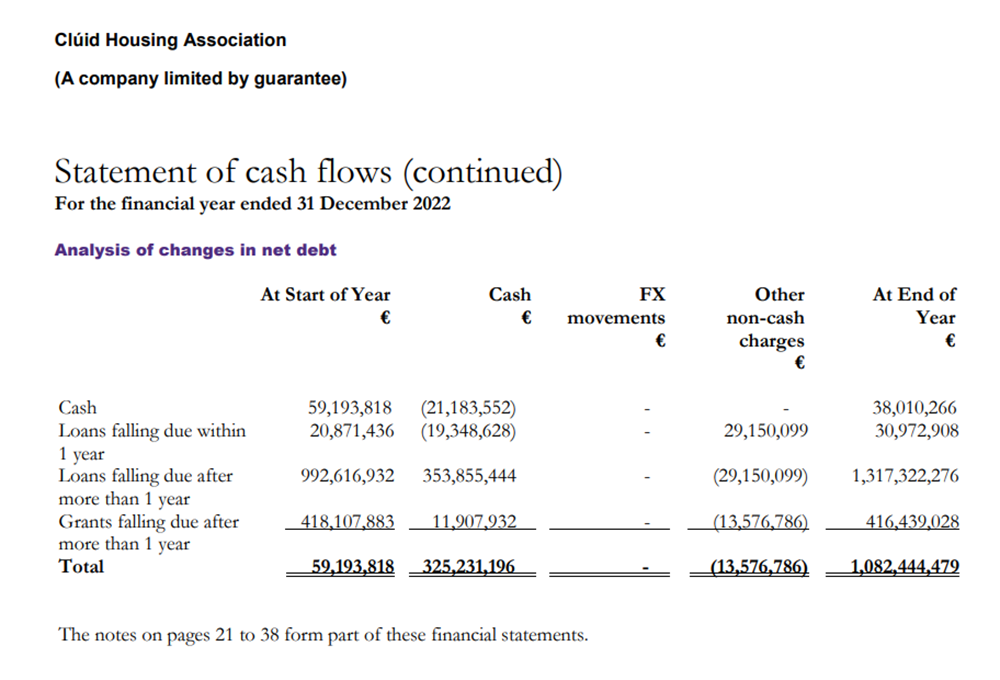

The amount of debt accumulated by the AHBs is striking. At the end of 2022, Clúid itself reported that the total value of loans carried was roughly €1.35 billion, with over €30 million in loans due in 2023.

That represented an increase of over €300 million in 12 months. The corresponding figure for the end of 2019 was €642 million, representing a doubling of debt in two years.

Total liabilities in 2022 amounted to €1.79 billion. The Grants repayable are the sums received from the state which are repayable at a very low interest rate by the AHB.

A similar debt situation is evident in the accounts lodged with the Companies Registration Office (CRO) and the Charity Regulator by the other main Approved Housing Bodies. Circle had outstanding loans of €61.3 million in 2017 but this had more than doubled to €143.4 million in 2022. Circle’s total liabilities amounted to €147.6 million.

There are no detailed financial statements available for the Co-operative Housing Ireland Society in either the CRO or with the Charity Regulator. This is despite a declared overall income of more than €50 million in 2022, of which over €28 million came from public funds. It currently has accumulated liabilities of €657.7 million.

The Co-operative Housing Society 2022 report does state that its earnings are currently covering repayments and that most of its loans are through the Housing Finance Agency and CALF, with 8% from the Bank of Ireland. It reported an increase in its debt from €420.3 million in 2021 to €566 million in 2022.

Another AHB, Oaklee, saw its debt rise to €224.5 million in 2023 from €33.75 million in 2017. It had total liabilities of €236.2 million. Oaklee has a wholly owned subsidiary, Acorn, which had debts of over €60 million.

Another body, Respond reported debts of almost €1.4 billion in 2022, which was up from €292 million in 2017.

The other Approved Housing Body that is part of the Housing Alliance, Tuath, reported a total debt of €1.77 billion in 2022 with €904 million owed to the banks. The overall debt had increased from €243.5 million in 2017. It has reported total liabilities of €1.38 billion.

One of the large AHBs that are not part of the Housing Alliance is Novas. Novas is unusual among the AHBs here in that it has its origins in a British left liberal NGO once known as Novas Scarman.

In 2005 Novas sold 11 hostels in order to raise a fund of £14 million which was to be used to pay for the refurbishment of a building called Arlington House. The hostels were sold but the funds were not available for the refurbishment due to “the fact that we do not have the £14 million as we have had other costs etc to pay off.’

Arlington Novas Ireland states that it became “independent from its founding UK charity parent company” in September 2005.

The head of Novas Scarman was Maria Donoghue Mills; she resigned after the UK regulator described “failures in management” which had undermined Novas “viability and reputation.” Donoghue Mills had been a director of the Irish Arlington Novas between 2002 and 2005. The story of the downfall of Novas Scarman would, you imagine, be sufficient to make Irish housing bodies wary of it as a model.

At the end of 2022, Arlington Novas had total liabilities of €37.8 million. It had debts of €35.2 million in 2002, compared to €21.3 million in 2016.

The total debt of the seven Approved Housing Bodies for whom we could find up to date information is almost €5 billion. The first report of the Approved Housing Bodies Regulatory Authority in 2023 put the overall debt of some 450 AHBs at €5.7 billion, the vast bulk of it held by the small number of large bodies we have examined. That is quite a large sum, especially if there appears to be a trend towards seeking private rather than public finance.

While the AHBs certainly have an important role to play in addressing the demand for affordable housing, the warning from Clúid regarding the dangers posed by that mounting debt needs to be addressed.

What also needs to be done is to ensure that liabilities to pension funds and other private agencies does not become another potential entry into the Irish housing market for people who certainly may not share the good intentions of the founders of the voluntary housing associations.